Last week’s orchestra compensation reports produced one of the most troubling instances in its nearly decade long history by way of discovering the Detroit Symphony Orchestra (DSO) implemented a policy designed to obfuscate their music director compensation. Moreover, when asked about the compensation data, the DSO refused to release the information, even though their music director provided his employer with permission to do exactly that.

For the sake of perspective, the lion’s share of professional orchestras have no problems releasing music director compensation figures, regardless if the conductor is paid as an employee, a private contractor, or a combination of both. To help illustrate this point, here’s a digital collage showing how the DSO’s peers have no difficulty complying with the Internal Revenue Service’s (IRS) executive compensation reporting requirements:

Why Are Orchestras Required To Report Executive Compensation?

Simply put, the IRS maintains the requirement in order to ensure nonprofit boards maintain fiduciary responsibility, enhance transparency, and help determine if executive compensation is not excessive. A report by Ward L. Thomas and James Bloom as part of a 1996 IRS continuing professional education initiative about reporting executive compensation for exempt organizations establishes these priorities in its opening paragraph (source | download).

Compensation of an exempt organization’s executives is some of the information most sought by the public on Form 990. Contributors do not like to see their hard-earned money used to pay the compensation of an executive who earns many times more than the contributors, especially where they believe the executive does not perform exempt function-related tasks commensurate with such salary…When a return that fails to report compensation fully and accurately is submitted, the Service’s ability to perform its duties, the public’s right to obtain meaningful information, and the public’s ability to police abuses are all impaired, since Form 990 is the main public source of such information.

Since professional orchestras in the United States are granted 501(c)(3) tax exempt status, they are required to adhere to these reporting practices.

In 2008, the IRS implemented a massive overhaul designed to enhance how nonprofits report executive compensation along with making it easier for nonprofits to comply, the guiding principles maintain what Thomas and Bloom outlined more than a decade prior (source | download).

The IRS extensively revised the format and content of the form based on three guiding principles: enhancing transparency, promoting tax compliance, and minimizing burden on the filing organization. Some of the major features of the new form include a new summary page, a new governance section, enhanced reporting of executive compensation and an organization’s relationships with insiders and other organizations…

Consequently, it is reasonable to summarize these positions by saying that potential donors have a right to reasonable transparency as applied to executive compensation for any nonprofit organization they are interested in supporting.

An Orchestra’s Unique Dual Executive Structure

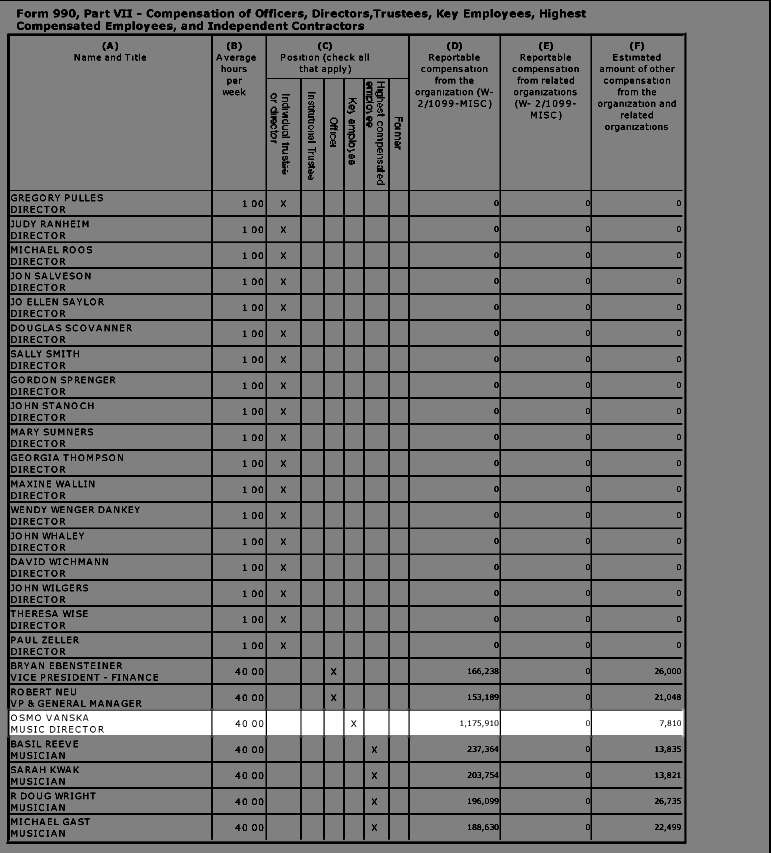

Although not universal, the vast majority of professional orchestras maintain a dual executive structure whereby there is one executive serving as the chief administrator for non-artistic functions and another executive responsible for artistic functions, the former is usually assigned titles such as CEO, President, or Executive Director while the latter is titled Music Director.

Both individuals report directly to the board of directors; in turn, the board is responsible for maintaining a written policy on setting and annually reviewing executive compensation.

An interesting wrinkle here is many music directors are paid as independent contractors as opposed to a traditional employee. Nonetheless, the IRS maintains long standing policies regarding this relationship via classifying these individuals as a disqualified person, this position was recently codified in a report from 2007 (source | download).

“A disqualified person is any person who was in a position to exercise substantial influence over the affairs of the tax exempt organization. See IRC §4958(f)(1).” – Report on Exempt Organizations Executive Compensation Compliance Project–Parts I and II, March 2007

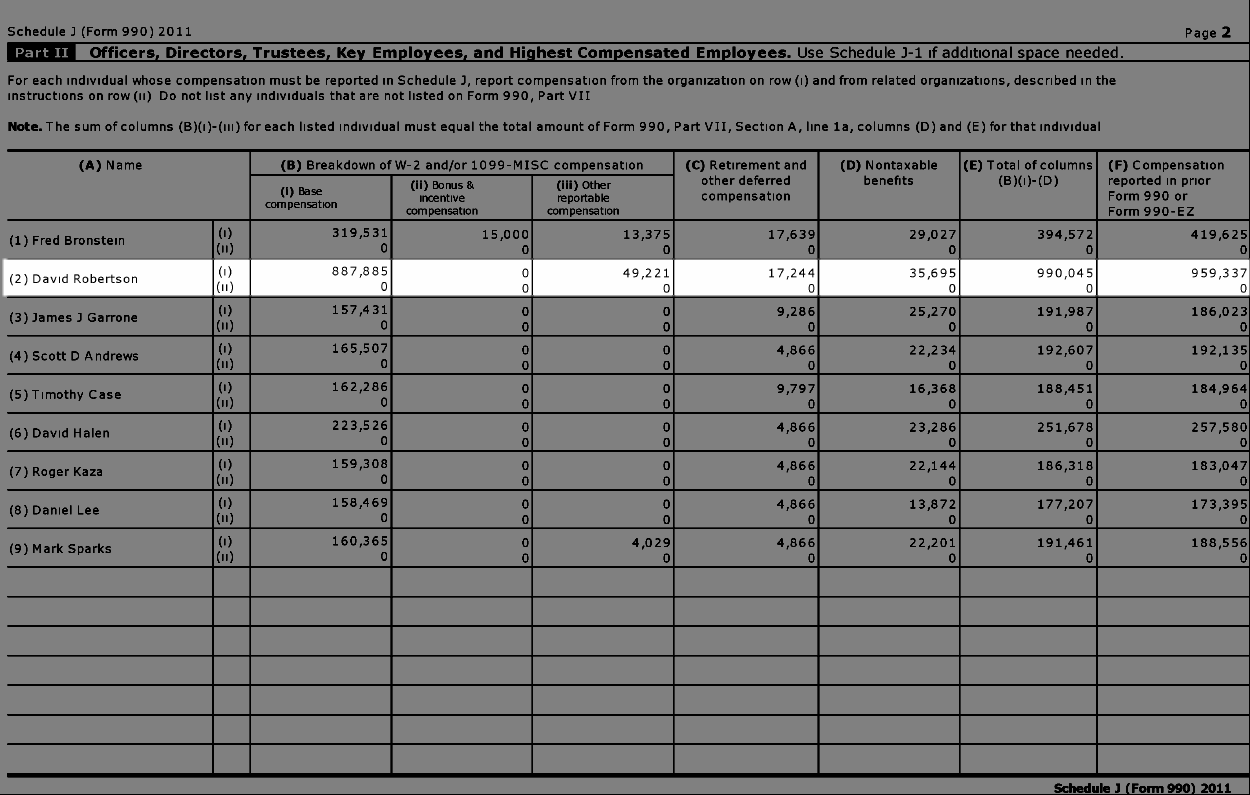

Accordingly, one would be hard pressed to argue against the notion that music directors do not “exercise substantial influence over the affairs of the tax exempt organization;” as a result, music director compensation has been routinely handled in the same way as traditional CEO compensation. Case in point, all but a handful of orchestras consistently reference the music director and CEO positions in their required compensation review disclosure statement; which is precisely what the DSO did in their Form 990 for the 2011/12 season (download – DSO compensation policy listing CEO and MD).

What Is Obfuscation And How Does It Apply To The DSO?

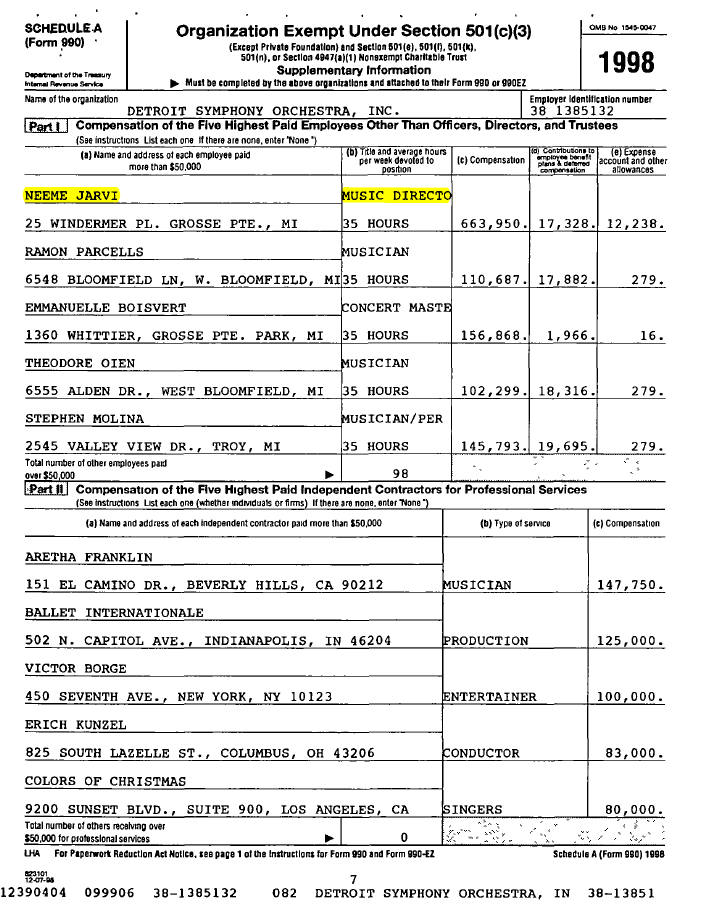

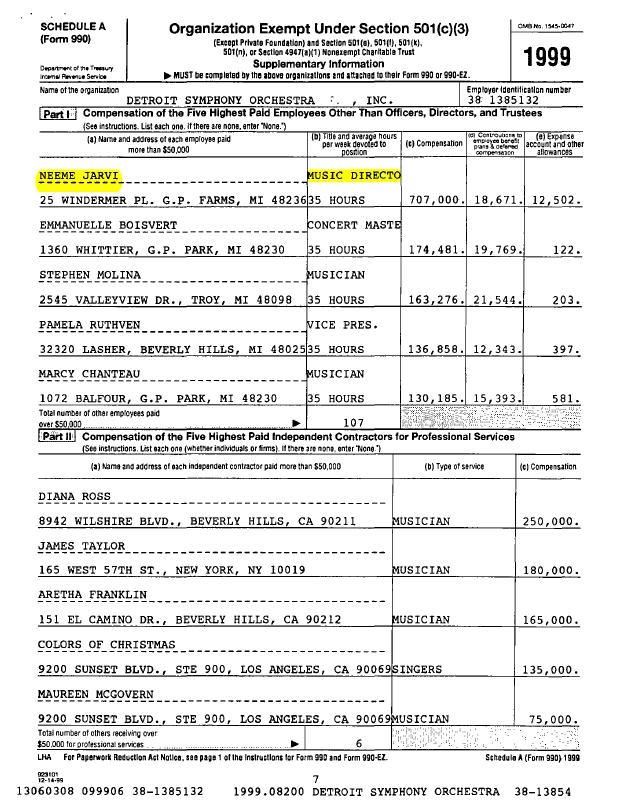

Although the DSO’s 2011/12 Form 990 references their music director by name, Leonard Slatkin, there is no entry in the document related to his compensation. Given that the DSO was dark for most of that season due to labor dispute related work stoppage, it was reasonable to hypothesize that the music director may not have been paid or even refused pay while the work stoppage was in place.

In order to determine if this was the case, I contacted Mr. Slatkin directly to inquire. His prompt reply indicated that he wasn’t certain and that I should contact the DSO’s Chief Financial Officer (CFO), he also mentioned that he would contact the CFO and let the individual know that the organization had his permission to release the information.

The DSO’s Director of Finance responded to the inquiry stating that the orchestra would not be releasing the information. Several communications later and the DSO’s official response was that their Board of Director’s Financial Information Distribution Policy prohibited releasing the music director’s compensation, even if the music director provides his or her permission to do so.

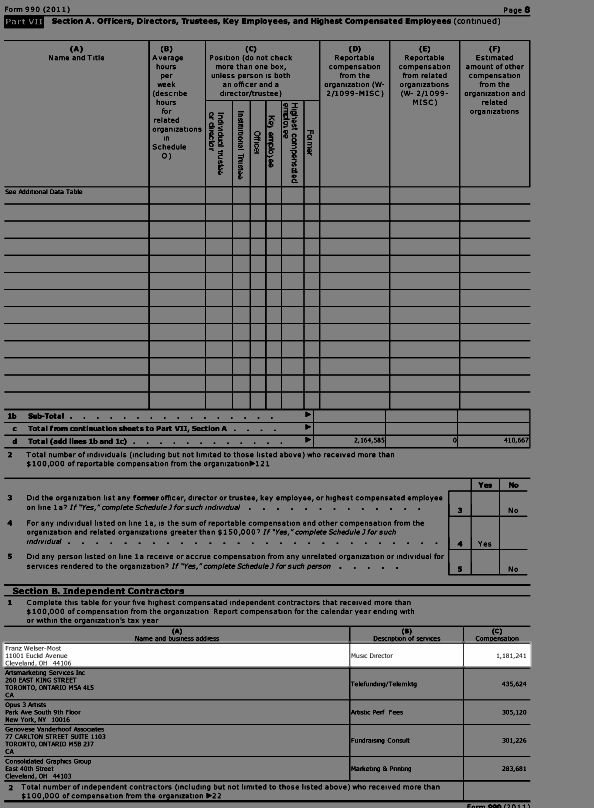

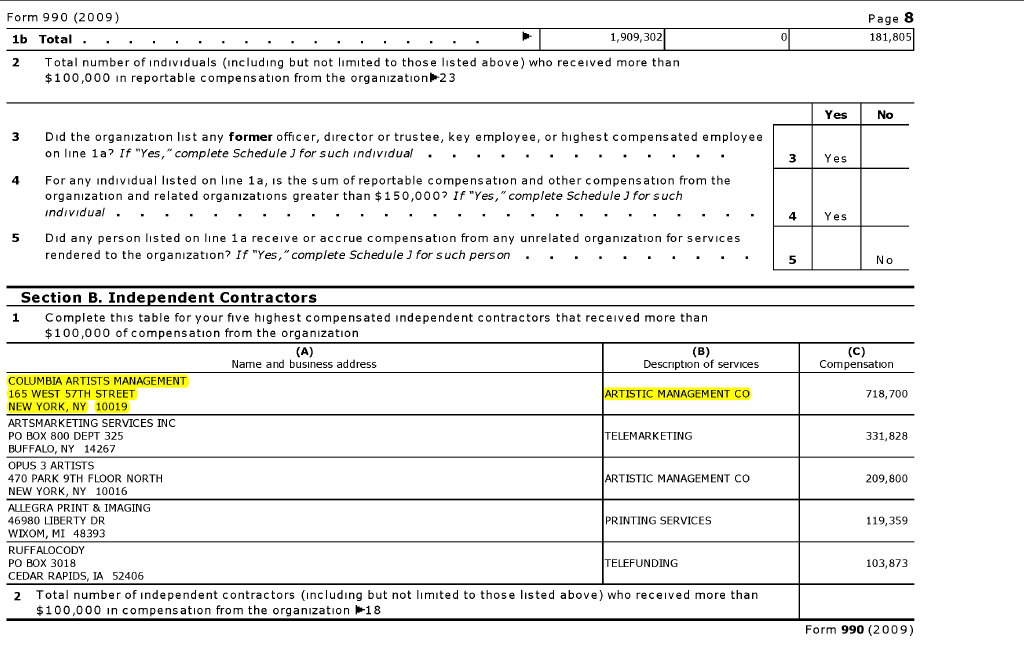

The DSO did indicate that some, but not all, of the music director compensation was included in a $718,700 disbursement to Columbia Artists Management, which represents Mr. Slatkin, as the organization’s highest paid independent contractor in the 2011/12 From 990 (source).

This is where obfuscation enters the picture; by including the music director compensation in a cumulative disbursement to an independent contractor, the organization circumvents IRS requirements for reporting executive compensation.

Running parallel to this is the organization’s decision to enact a financial disclosure policy designed to deflect requests for clarification.

Perhaps unsurprisingly, it isn’t difficult to see that these actions may be interpreted as a sign that the DSO is somehow exempt from the ethical guidelines related to reporting nonprofit executive compensation. In short, the rules don’t apply to them.

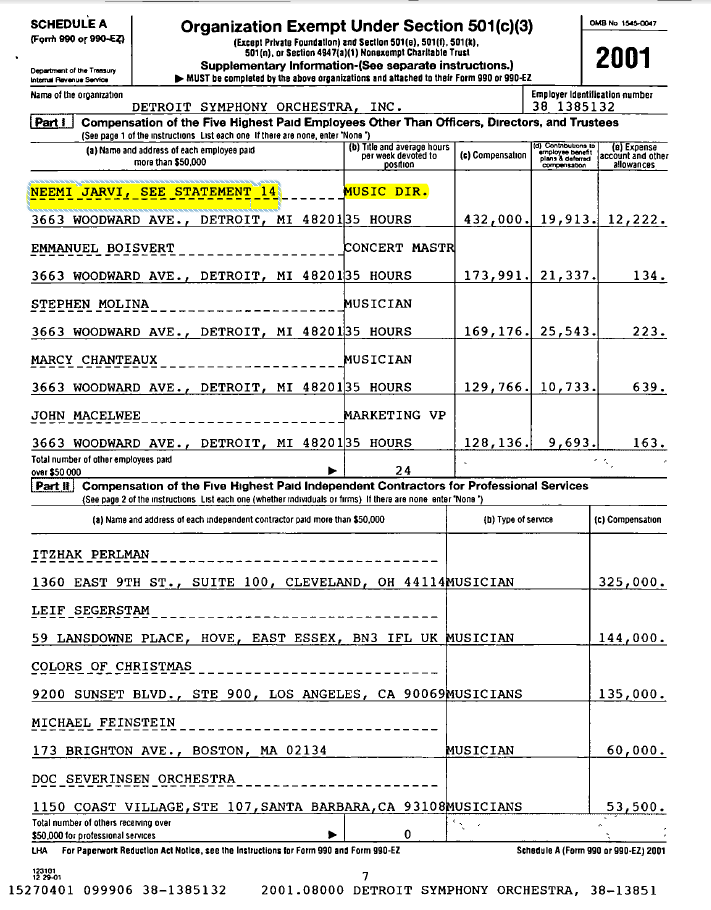

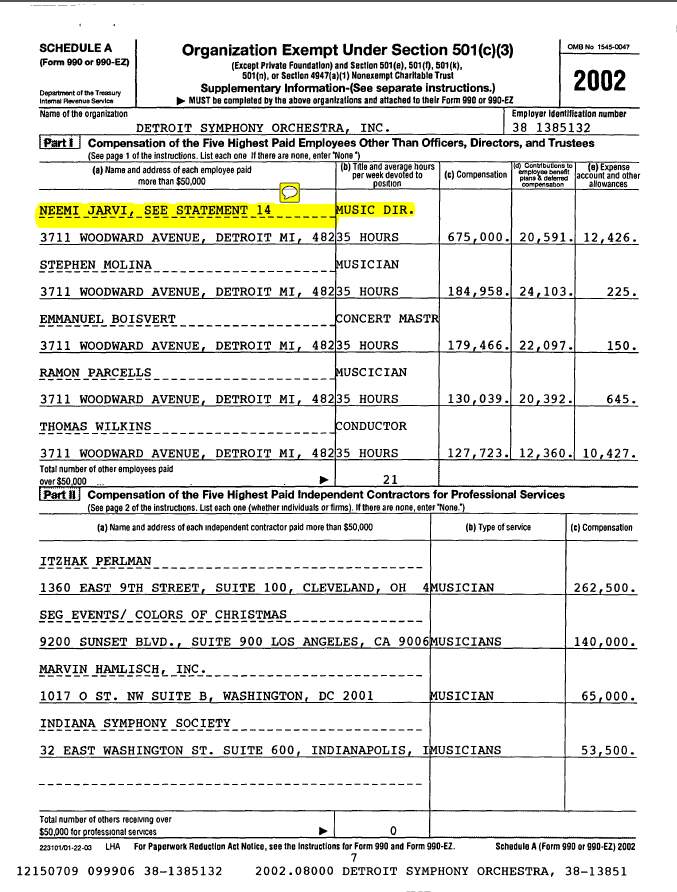

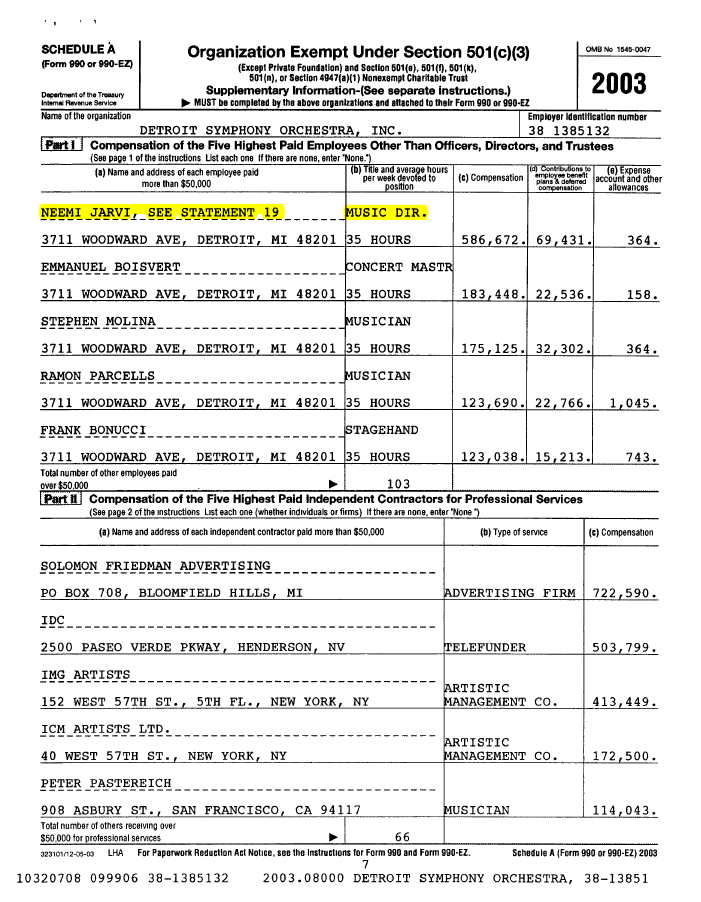

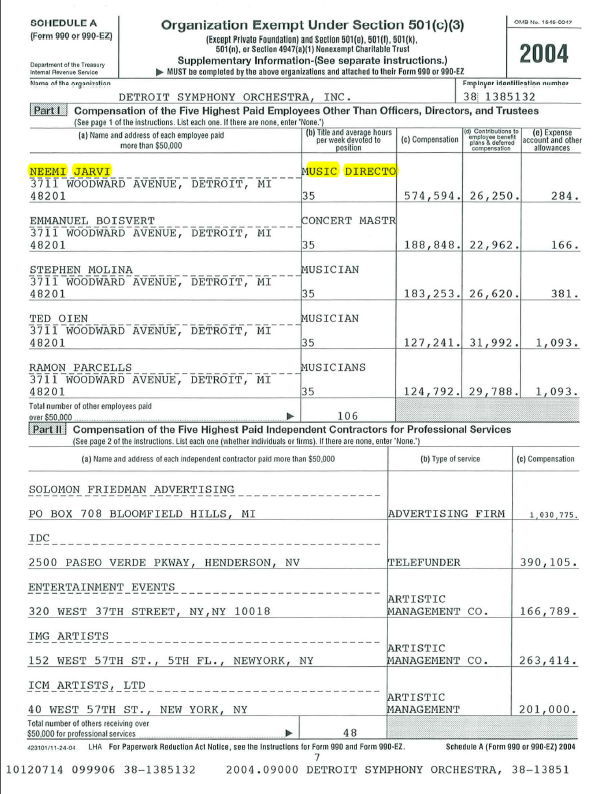

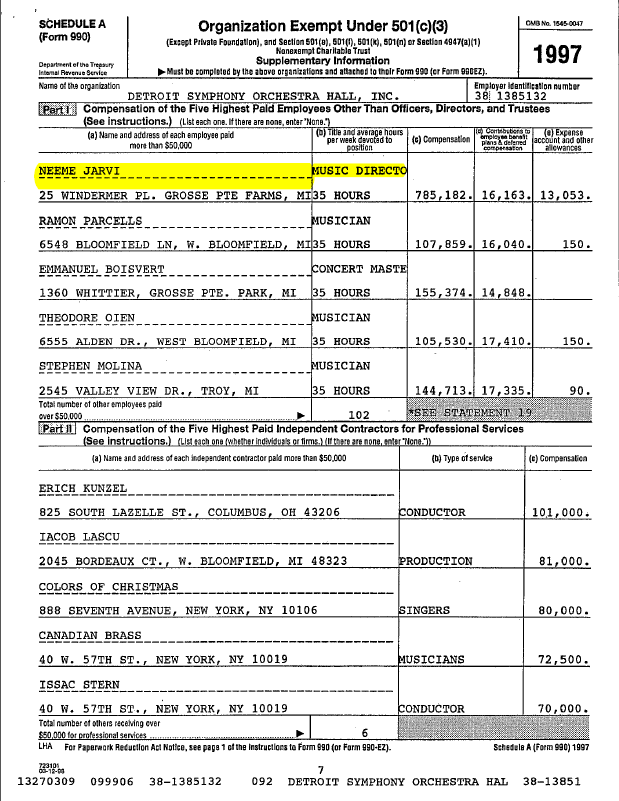

As it turns out, the vast majority of the DSO’s peers have a long standing history of compliance and the DSO’s record of financial returns demonstrates that the institution maintained a similar position, as illustrated with these eight examples from the 1998/99 season through 2004/05 season (the DSO was without a music director during the 05/06, 06/07, and 07/08 seasons).

Conclusions

The DSOs actions only reinforce that the while the institution professes a commitment to transparency, their actions indicate otherwise. Moreover, their conduct has the very real potential for damaging the reputation of the entire field by sowing the seeds of donor mistrust, thereby producing a negative impact on individual and institutional giving.

Consequently, the real concerns here circle back to one of the cornerstones behind why the IRS requires executive compensation disclose in the first place: maintaining public trust.

The DSO’s decision to create a policy designed to obfuscate music director compensation comes across as a page out of “the rules don’t apply to us” behavior exhibited by financial institution boards during the Troubled Asset Relief Program (TARP) saga but in the end, the DSO should make things right by revising its reporting and disclosure policies to align with their peers and adhere to IRS guidelines; likewise, they need to amend any returns that currently fail to meet this threshold by providing missing details related to music director compensation.

At the time this article was published, the DSO refuses to discuss the issue and instead, has opted to release the following statement via DSO Patron Communications and Public Relations manager Gabrielle Poshadlo:

After reviewing the DSO Board of Director’s Financial Information Distribution Policy with our CEO [Anne Parsons] and EVP [Paul Hogle], I regret to inform you that we are unable to disclose information that is not included in our Audited Form 990 and/or Annual Report.

And there you have it.

Apparently, the death of ethical governance and adherence to IRS regulations is as simple as passing an internal board policy.

Bonus Resources

In order to help provide as much reference material as possible, you can download a resource kit containing all of the DSO’s IRS Form 990 returns covering the 1997/98 through 2011/12 seasons (with the exception of the 2007/08 season, which I did not have on file).

Moreover, the documents were processed via Adobe Acrobat’s Optical Text Recognition (OCR) tools, thereby rendering each Form 990 keyword searchable. Please note that liberty has been exercised by way of highlighting content related to today’s post in each of the respective 990 documents. The zip file also contains copies of the IRS documentation referenced in today’s article.

[ilink url=”https://adaptistration.com/wp-content/uploads/DSO-990-and-Reference-Material.zip” style=”download”]Download the resource kit (26.3MB zip file)[/ilink]

{kind=link}

Shameful and embarrassing. Question: Can the public request the IRS audit an exempt organization due to dubious reporting practices?

Ideally, this won’t be necessary thanks to the DSO amending their policy and providing the information, however, the IRS does maintain a process for individuals believing a tax-exempt organization is in potential noncompliance with the tax law. that process is detailed here.

Why do I have a feeling the DSO will not be alone in this practice in a few years?

I genuinely hope that won’t be the case.

Can a music director contractually request that their salary not be made public in this manner?

Now there’s the big question and it treads on a number of issues that typically transpire as part of the music director’s individual work contract. The short answer is a conductor can request whatever s/he wants, regardless the rationale. Whether or not the institution can or will provide it is another story and guidelines such as the IRS executive compensation reporting requirements help determine how orchestras should approach these issues. the far more common point of negotiation is how the music director will be employed and how compensation disbursements transpire. For instance, will the individual be classified as an employee, independent contract, or both? Many conductors in larger budget orchestras establish their own corporation (s-Corp, LLC, etc.). It’s usually self evident how this arrangement has been structured via an orchestra’s Form 990, for instance Michael Tilson Thomas’s payments as independent contractor are disbursed to his corporation (MTT Inc) and Christoph Eschenbach has his compensation disbursed care of an accounting firm.

Ethics were alive?

Yes, alive and kicking in fact, at least when it comes to this topic. Don’t forget that the majority of orchestras have no problem reporting music director compensation nor have they adopted internal policies designed to obfuscate the data.